| Type: | Package |

| Title: | Processing of Model Parameters |

| Version: | 0.29.2 |

| Maintainer: | Daniel Lüdecke <officialeasystats@gmail.com> |

| Description: | Utilities for processing the parameters of various statistical models. Beyond computing p values, CIs, and other indices for a wide variety of models (see list of supported models using the function 'insight::supported_models()'), this package implements features like bootstrapping or simulating of parameters and models, feature reduction (feature extraction and variable selection) as well as functions to describe data and variable characteristics (e.g. skewness, kurtosis, smoothness or distribution). |

| License: | GPL-3 |

| URL: | https://easystats.github.io/parameters/ |

| BugReports: | https://github.com/easystats/parameters/issues |

| Depends: | R (≥ 3.6) |

| Imports: | bayestestR (≥ 0.18.1), datawizard (≥ 1.3.1), insight (≥ 1.5.1), graphics, methods, stats, utils |

| Suggests: | AER, afex, aod, BayesFactor (≥ 0.9.12-4.7), BayesFM, bbmle, BSDA, betareg, BH, biglm, blme, boot, brglm2, brms, broom, broom.mixed, cAIC4, car, carData, cgam, ClassDiscovery, clubSandwich, cluster, cobalt, coda, correlation (≥ 0.8.8), coxme, cplm, curl, dbscan, did, discovr, distributional, domir (≥ 0.2.0), drc, DRR, effectsize (≥ 1.0.1), EGAnet, emmeans (≥ 1.7.0), epiR, estimatr, factoextra, FactoMineR, faraway, fastICA, fixest, fpc, gam, gamlss, gee, geepack, ggplot2, GLMMadaptive, glmmTMB (≥ 1.1.12), glmtoolbox, GPArotation, gt, haven, httr2, Hmisc, ivreg, knitr, lavaan, lavaan.mi, lcmm, lfe, lm.beta, lme4, lmerTest, lmtest, logistf, logitr, logspline, lqmm, M3C, marginaleffects (≥ 0.29.0), modelbased (≥ 0.9.0), MASS, Matrix, mclogit, mclust, MCMCglmm, mediation, merDeriv, metaBMA, metafor, mfx, mgcv, mice (≥ 3.17.0), mmrm, multcomp, MuMIn, mvtnorm, NbClust, nFactors, nestedLogit, nlme, nnet, openxlsx, ordinal, panelr, pbkrtest, PCDimension, performance (≥ 0.14.0), plm, PMCMRplus, poorman, posterior, PROreg (≥ 1.3.0), pscl, psych, pvclust, quantreg, randomForest, RcppEigen, rmarkdown, rms, rstan, rstanarm, sampleSelection, sandwich, see (≥ 0.8.1), serp, sparsepca, survey, survival, svylme, testthat (≥ 3.2.1), tidyselect, tinytable (≥ 0.13.0), TMB, truncreg, vdiffr, VGAM, WeightIt (≥ 1.2.0), withr, WRS2 |

| VignetteBuilder: | knitr |

| Encoding: | UTF-8 |

| Language: | en-US |

| Config/testthat/edition: | 3 |

| Config/testthat/parallel: | false |

| Config/Needs/website: | easystats/easystatstemplate |

| Config/Needs/check: | stan-dev/cmdstanr |

| Config/rcmdcheck/ignore-inconsequential-notes: | true |

| Config/roxygen2/version: | 8.0.0 |

| NeedsCompilation: | no |

| Packaged: | 2026-06-28 20:12:36 UTC; Daniel |

| Author: | Daniel Lüdecke  [aut, cre],

Dominique Makowski

[aut],

Mattan S. Ben-Shachar

[aut],

Indrajeet Patil

[aut],

Søren Højsgaard [aut],

Brenton M. Wiernik

[aut],

Zen J. Lau [ctb],

Vincent Arel-Bundock

[ctb],

Jeffrey Girard

[ctb],

Christina Maimone [rev],

Niels Ohlsen [rev],

Douglas Ezra Morrison

[ctb],

Joseph Luchman

[ctb]

[aut, cre],

Dominique Makowski

[aut],

Mattan S. Ben-Shachar

[aut],

Indrajeet Patil

[aut],

Søren Højsgaard [aut],

Brenton M. Wiernik

[aut],

Zen J. Lau [ctb],

Vincent Arel-Bundock

[ctb],

Jeffrey Girard

[ctb],

Christina Maimone [rev],

Niels Ohlsen [rev],

Douglas Ezra Morrison

[ctb],

Joseph Luchman

[ctb] |

| Repository: | CRAN |

| Date/Publication: | 2026-06-28 23:20:02 UTC |

parameters: Extracting, Computing and Exploring the Parameters of Statistical Models using R

Description

parameters' primary goal is to provide utilities for processing the parameters of various statistical models (see here for a list of supported models). Beyond computing p-values, CIs, Bayesian indices and other measures for a wide variety of models, this package implements features like bootstrapping of parameters and models, feature reduction (feature extraction and variable selection), or tools for data reduction like functions to perform cluster, factor or principal component analysis.

Another important goal of the parameters package is to facilitate and streamline the process of reporting results of statistical models, which includes the easy and intuitive calculation of standardized estimates or robust standard errors and p-values. parameters therefor offers a simple and unified syntax to process a large variety of (model) objects from many different packages.

References: Lüdecke et al. (2020) doi:10.21105/joss.02445

Author(s)

Maintainer: Daniel Lüdecke officialeasystats@gmail.com (ORCID)

Authors:

Daniel Lüdecke officialeasystats@gmail.com (ORCID)

Dominique Makowski dom.makowski@gmail.com (ORCID)

Mattan S. Ben-Shachar matanshm@post.bgu.ac.il (ORCID)

Indrajeet Patil patilindrajeet.science@gmail.com (ORCID)

Søren Højsgaard sorenh@math.aau.dk

Brenton M. Wiernik brenton@wiernik.org (ORCID)

Other contributors:

Zen J. Lau zenjuen.lau@ntu.edu.sg [contributor]

Vincent Arel-Bundock vincent.arel-bundock@umontreal.ca (ORCID) [contributor]

Jeffrey Girard me@jmgirard.com (ORCID) [contributor]

Christina Maimone christina.maimone@northwestern.edu [reviewer]

Niels Ohlsen [reviewer]

Douglas Ezra Morrison dmorrison01@ucla.edu (ORCID) [contributor]

Joseph Luchman jluchman@gmail.com (ORCID) [contributor]

See Also

Useful links:

Report bugs at https://github.com/easystats/parameters/issues

help-functions

Description

help-functions

Usage

.data_frame(...)

Safe transformation from factor/character to numeric

Description

Safe transformation from factor/character to numeric

Usage

.factor_to_dummy(x)

for models with zero-inflation component, return required component of model-summary

Description

for models with zero-inflation component, return required component of model-summary

Usage

.filter_component(dat, component)

Bartlett, Anderson and Lawley Procedures

Description

Bartlett, Anderson and Lawley Procedures

Usage

.n_factors_bartlett(eigen_values = NULL, model = "factors", nobs = NULL)

Bentler and Yuan's Procedure

Description

Bentler and Yuan's Procedure

Usage

.n_factors_bentler(eigen_values = NULL, model = "factors", nobs = NULL)

Cattell-Nelson-Gorsuch CNG Indices

Description

Cattell-Nelson-Gorsuch CNG Indices

Usage

.n_factors_cng(eigen_values = NULL, model = "factors")

Multiple Regression Procedure

Description

Multiple Regression Procedure

Usage

.n_factors_mreg(eigen_values = NULL, model = "factors")

Non Graphical Cattell's Scree Test

Description

Non Graphical Cattell's Scree Test

Usage

.n_factors_scree(eigen_values = NULL, model = "factors")

Standard Error Scree and Coefficient of Determination Procedures

Description

Standard Error Scree and Coefficient of Determination Procedures

Usage

.n_factors_sescree(eigen_values = NULL, model = "factors")

Model bootstrapping

Description

Bootstrap a statistical model n times to return a data frame of estimates.

Usage

bootstrap_model(model, iterations = 1000, ...)

## Default S3 method:

bootstrap_model(

model,

iterations = 1000,

type = "ordinary",

parallel = "no",

n_cpus = 1,

cluster = NULL,

verbose = FALSE,

...

)

Arguments

model |

Statistical model. |

iterations |

The number of draws to simulate/bootstrap. |

... |

Arguments passed to or from other methods. |

type |

Character string specifying the type of bootstrap. For mixed models

of class |

parallel |

The type of parallel operation to be used (if any). |

n_cpus |

Number of processes to be used in parallel operation. |

cluster |

Optional cluster when |

verbose |

Toggle warnings and messages. |

Details

By default, boot::boot() is used to generate bootstraps from

the model data, which are then used to update() the model, i.e. refit

the model with the bootstrapped samples. For merMod objects (lme4)

or models from glmmTMB, the lme4::bootMer() function is used to

obtain bootstrapped samples. bootstrap_parameters() summarizes the

bootstrapped model estimates.

Value

A data frame of bootstrapped estimates.

Using with emmeans

The output can be passed directly to the various functions from the

emmeans package, to obtain bootstrapped estimates, contrasts, simple

slopes, etc. and their confidence intervals. These can then be passed to

model_parameter() to obtain standard errors, p-values, etc. (see

example).

Note that that p-values returned here are estimated under the assumption of translation equivariance: that shape of the sampling distribution is unaffected by the null being true or not. If this assumption does not hold, p-values can be biased, and it is suggested to use proper permutation tests to obtain non-parametric p-values.

See Also

bootstrap_parameters(), simulate_model(), simulate_parameters()

Examples

model <- lm(mpg ~ wt + factor(cyl), data = mtcars)

b <- bootstrap_model(model)

print(head(b))

est <- emmeans::emmeans(b, consec ~ cyl)

print(model_parameters(est))

Parameters bootstrapping

Description

Compute bootstrapped parameters and their related indices such as Confidence Intervals (CI) and p-values.

Usage

bootstrap_parameters(model, ...)

## Default S3 method:

bootstrap_parameters(

model,

iterations = 1000,

centrality = "median",

ci = 0.95,

ci_method = "quantile",

test = "p-value",

...

)

Arguments

model |

Statistical model. |

... |

Arguments passed to other methods, like |

iterations |

The number of draws to simulate/bootstrap. |

centrality |

The point-estimates (centrality indices) to compute. Character

(vector) or list with one or more of these options: |

ci |

Value or vector of probability of the CI (between 0 and 1)

to be estimated. Default to |

ci_method |

The type of index used for Credible Interval. Can be |

test |

The indices to compute. Character (vector) with one or more of

these options: |

Details

This function first calls bootstrap_model() to generate

bootstrapped coefficients. The resulting replicated for each coefficient

are treated as "distribution", and is passed to bayestestR::describe_posterior()

to calculate the related indices defined in the "test" argument.

Note that that p-values returned here are estimated under the assumption of translation equivariance: that shape of the sampling distribution is unaffected by the null being true or not. If this assumption does not hold, p-values can be biased, and it is suggested to use proper permutation tests to obtain non-parametric p-values.

Value

A data frame summarizing the bootstrapped parameters.

Using with emmeans

The output can be passed directly to the various functions from the

emmeans package, to obtain bootstrapped estimates, contrasts, simple

slopes, etc. and their confidence intervals. These can then be passed to

model_parameter() to obtain standard errors, p-values, etc. (see

example).

Note that that p-values returned here are estimated under the assumption of translation equivariance: that shape of the sampling distribution is unaffected by the null being true or not. If this assumption does not hold, p-values can be biased, and it is suggested to use proper permutation tests to obtain non-parametric p-values.

References

Davison, A. C., & Hinkley, D. V. (1997). Bootstrap methods and their application (Vol. 1). Cambridge university press.

See Also

bootstrap_model(), simulate_parameters(), simulate_model()

Examples

set.seed(2)

model <- lm(Sepal.Length ~ Species * Petal.Width, data = iris)

b <- bootstrap_parameters(model)

print(b)

# different type of bootstrapping

set.seed(2)

b <- bootstrap_parameters(model, type = "balanced")

print(b)

est <- emmeans::emmeans(b, trt.vs.ctrl ~ Species)

print(model_parameters(est))

Confidence Intervals (CI)

Description

ci() attempts to return confidence intervals of model parameters.

Usage

## Default S3 method:

ci(

x,

ci = 0.95,

dof = NULL,

method = NULL,

iterations = 500,

component = "all",

vcov = NULL,

vcov_args = NULL,

verbose = TRUE,

...

)

Arguments

x |

A statistical model. |

ci |

Confidence Interval (CI) level. Default to |

dof |

Number of degrees of freedom to be used when calculating

confidence intervals. If |

method |

Method for computing degrees of freedom for confidence

intervals (CI) and the related p-values. Allowed are following options (which

vary depending on the model class): |

iterations |

The number of bootstrap replicates. Only applies to models

of class |

component |

Model component for which parameters should be shown. See

the documentation for your object's class in |

vcov |

Variance-covariance matrix used to compute uncertainty estimates (e.g., for robust standard errors). This argument accepts a covariance matrix, a function which returns a covariance matrix, or a string which identifies the function to be used to compute the covariance matrix.

|

vcov_args |

List of arguments to be passed to the function identified by

the |

verbose |

Toggle warnings and messages. |

... |

Additional arguments passed down to the underlying functions.

E.g., arguments like |

Value

A data frame containing the CI bounds.

Confidence intervals and approximation of degrees of freedom

There are different ways of approximating the degrees of freedom depending

on different assumptions about the nature of the model and its sampling

distribution. The ci_method argument modulates the method for computing degrees

of freedom (df) that are used to calculate confidence intervals (CI) and the

related p-values. Following options are allowed, depending on the model

class:

Classical methods:

Classical inference is generally based on the Wald method. The Wald approach to inference computes a test statistic by dividing the parameter estimate by its standard error (Coefficient / SE), then comparing this statistic against a t- or normal distribution. This approach can be used to compute CIs and p-values.

"wald":

Applies to non-Bayesian models. For linear models, CIs computed using the Wald method (SE and a t-distribution with residual df); p-values computed using the Wald method with a t-distribution with residual df. For other models, CIs computed using the Wald method (SE and a normal distribution); p-values computed using the Wald method with a normal distribution.

"normal"

Applies to non-Bayesian models. Compute Wald CIs and p-values, but always use a normal distribution.

"residual"

Applies to non-Bayesian models. Compute Wald CIs and p-values, but always use a t-distribution with residual df when possible. If the residual df for a model cannot be determined, a normal distribution is used instead.

Methods for mixed models:

Compared to fixed effects (or single-level) models, determining appropriate df for Wald-based inference in mixed models is more difficult. See the R GLMM FAQ for a discussion.

Several approximate methods for computing df are available, but you should

also consider instead using profile likelihood ("profile") or bootstrap ("boot")

CIs and p-values instead.

"satterthwaite"

Applies to linear mixed models. CIs computed using the Wald method (SE and a t-distribution with Satterthwaite df); p-values computed using the Wald method with a t-distribution with Satterthwaite df.

"kenward"

Applies to linear mixed models. CIs computed using the Wald method (Kenward-Roger SE and a t-distribution with Kenward-Roger df); p-values computed using the Wald method with Kenward-Roger SE and t-distribution with Kenward-Roger df.

"ml1"

Applies to linear mixed models. CIs computed using the Wald method (SE and a t-distribution with m-l-1 approximated df); p-values computed using the Wald method with a t-distribution with m-l-1 approximated df. See

ci_ml1().

"betwithin"

Applies to linear mixed models and generalized linear mixed models. CIs computed using the Wald method (SE and a t-distribution with between-within df); p-values computed using the Wald method with a t-distribution with between-within df. See

ci_betwithin().

Likelihood-based methods:

Likelihood-based inference is based on comparing the likelihood for the

maximum-likelihood estimate to the the likelihood for models with one or more

parameter values changed (e.g., set to zero or a range of alternative values).

Likelihood ratios for the maximum-likelihood and alternative models are compared

to a \chi-squared distribution to compute CIs and p-values.

"profile"

Applies to non-Bayesian models of class

glm,polr,merModorglmmTMB. CIs computed by profiling the likelihood curve for a parameter, using linear interpolation to find where likelihood ratio equals a critical value; p-values computed using the Wald method with a normal-distribution (note: this might change in a future update!)

"uniroot"

Applies to non-Bayesian models of class

glmmTMB. CIs computed by profiling the likelihood curve for a parameter, using root finding to find where likelihood ratio equals a critical value; p-values computed using the Wald method with a normal-distribution (note: this might change in a future update!)

Methods for bootstrapped or Bayesian models:

Bootstrap-based inference is based on resampling and refitting the model to the resampled datasets. The distribution of parameter estimates across resampled datasets is used to approximate the parameter's sampling distribution. Depending on the type of model, several different methods for bootstrapping and constructing CIs and p-values from the bootstrap distribution are available.

For Bayesian models, inference is based on drawing samples from the model posterior distribution.

"quantile" (or "eti")

Applies to all models (including Bayesian models). For non-Bayesian models, only applies if

bootstrap = TRUE. CIs computed as equal tailed intervals using the quantiles of the bootstrap or posterior samples; p-values are based on the probability of direction. SeebayestestR::eti().

"hdi"

Applies to all models (including Bayesian models). For non-Bayesian models, only applies if

bootstrap = TRUE. CIs computed as highest density intervals for the bootstrap or posterior samples; p-values are based on the probability of direction. SeebayestestR::hdi().

"bci" (or "bcai")

Applies to all models (including Bayesian models). For non-Bayesian models, only applies if

bootstrap = TRUE. CIs computed as bias corrected and accelerated intervals for the bootstrap or posterior samples; p-values are based on the probability of direction. SeebayestestR::bci().

"si"

Applies to Bayesian models with proper priors. CIs computed as support intervals comparing the posterior samples against the prior samples; p-values are based on the probability of direction. See

bayestestR::si().

"boot"

Applies to non-Bayesian models of class

merMod. CIs computed using parametric bootstrapping (simulating data from the fitted model); p-values computed using the Wald method with a normal-distribution) (note: this might change in a future update!).

For all iteration-based methods other than "boot"

("hdi", "quantile", "ci", "eti", "si", "bci", "bcai"),

p-values are based on the probability of direction (bayestestR::p_direction()),

which is converted into a p-value using bayestestR::pd_to_p().

Model components

Possible values for the component argument depend on the model class.

Following are valid options:

-

"all": returns all model components, applies to all models, but will only have an effect for models with more than just the conditional model component. -

"conditional": only returns the conditional component, i.e. "fixed effects" terms from the model. Will only have an effect for models with more than just the conditional model component. -

"smooth_terms": returns smooth terms, only applies to GAMs (or similar models that may contain smooth terms). -

"zero_inflated"(or"zi"): returns the zero-inflation component. -

"dispersion": returns the dispersion model component. This is common for models with zero-inflation or that can model the dispersion parameter. -

"instruments": for instrumental-variable or some fixed effects regression, returns the instruments. -

"nonlinear": for non-linear models (like models of classnlmerModornls), returns staring estimates for the nonlinear parameters. -

"correlation": for models with correlation-component, likegls, the variables used to describe the correlation structure are returned.

Special models

Some model classes also allow rather uncommon options. These are:

-

mhurdle:

"infrequent_purchase","ip", and"auxiliary" -

BGGM:

"correlation"and"intercept" -

BFBayesFactor, glmx:

"extra" -

averaging:

"conditional"and"full" -

mjoint:

"survival" -

mfx:

"precision","marginal" -

betareg, DirichletRegModel:

"precision" -

mvord:

"thresholds"and"correlation" -

clm2:

"scale" -

selection:

"selection","outcome", and"auxiliary" -

lavaan: One or more of

"regression","correlation","loading","variance","defined", or"mean". Can also be"all"to include all components.

For models of class brmsfit (package brms), even more options are

possible for the component argument, which are not all documented in detail

here.

Examples

data(qol_cancer)

model <- lm(QoL ~ time + age + education, data = qol_cancer)

# regular confidence intervals

ci(model)

# using heteroscedasticity-robust standard errors

ci(model, vcov = "HC3")

library(parameters)

data(Salamanders, package = "glmmTMB")

model <- glmmTMB::glmmTMB(

count ~ spp + mined + (1 | site),

ziformula = ~mined,

family = poisson(),

data = Salamanders

)

ci(model)

ci(model, component = "zi")

Between-within approximation for SEs, CIs and p-values

Description

Approximation of degrees of freedom based on a "between-within" heuristic.

Usage

ci_betwithin(model, ci = 0.95, ...)

dof_betwithin(model)

p_value_betwithin(model, dof = NULL, ...)

Arguments

model |

A mixed model. |

ci |

Confidence Interval (CI) level. Default to |

... |

Additional arguments passed down to the underlying functions.

E.g., arguments like |

dof |

Degrees of Freedom. |

Details

Small Sample Cluster corrected Degrees of Freedom

Inferential statistics (like p-values, confidence intervals and

standard errors) may be biased in mixed models when the number of clusters

is small (even if the sample size of level-1 units is high). In such cases

it is recommended to approximate a more accurate number of degrees of freedom

for such inferential statistics (see Li and Redden 2015). The

Between-within denominator degrees of freedom approximation is

recommended in particular for (generalized) linear mixed models with repeated

measurements (longitudinal design). dof_betwithin() implements a heuristic

based on the between-within approach. Note that this implementation

does not return exactly the same results as shown in Li and Redden 2015,

but similar.

Degrees of Freedom for Longitudinal Designs (Repeated Measures)

In particular for repeated measure designs (longitudinal data analysis),

the between-within heuristic is likely to be more accurate than simply

using the residual or infinite degrees of freedom, because dof_betwithin()

returns different degrees of freedom for within-cluster and between-cluster

effects.

Value

A data frame.

References

Elff, M.; Heisig, J.P.; Schaeffer, M.; Shikano, S. (2019). Multilevel Analysis with Few Clusters: Improving Likelihood-based Methods to Provide Unbiased Estimates and Accurate Inference, British Journal of Political Science.

Li, P., Redden, D. T. (2015). Comparing denominator degrees of freedom approximations for the generalized linear mixed model in analyzing binary outcome in small sample cluster-randomized trials. BMC Medical Research Methodology, 15(1), 38. doi:10.1186/s12874-015-0026-x

See Also

dof_betwithin() is a small helper-function to calculate approximated

degrees of freedom of model parameters, based on the "between-within" heuristic.

Examples

if (require("lme4")) {

data(sleepstudy)

model <- lmer(Reaction ~ Days + (1 + Days | Subject), data = sleepstudy)

dof_betwithin(model)

p_value_betwithin(model)

}

Kenward-Roger approximation for SEs, CIs and p-values

Description

An approximate F-test based on the Kenward-Roger (1997) approach.

Usage

ci_kenward(model, ci = 0.95, ...)

dof_kenward(model)

p_value_kenward(model, dof = NULL)

se_kenward(model, ...)

Arguments

model |

A statistical model. |

ci |

Confidence Interval (CI) level. Default to |

... |

Additional arguments passed down to the underlying functions.

E.g., arguments like |

dof |

Degrees of Freedom. |

Details

Inferential statistics (like p-values, confidence intervals and

standard errors) may be biased in mixed models when the number of clusters

is small (even if the sample size of level-1 units is high). In such cases

it is recommended to approximate a more accurate number of degrees of freedom

for such inferential statistics. Unlike simpler approximation heuristics

like the "m-l-1" rule (dof_ml1), the Kenward-Roger approximation is

also applicable in more complex multilevel designs, e.g. with cross-classified

clusters. However, the "m-l-1" heuristic also applies to generalized

mixed models, while approaches like Kenward-Roger or Satterthwaite are limited

to linear mixed models only.

Value

A data frame.

References

Kenward, M. G., & Roger, J. H. (1997). Small sample inference for fixed effects from restricted maximum likelihood. Biometrics, 983-997.

See Also

dof_kenward() and se_kenward() are small helper-functions

to calculate approximated degrees of freedom and standard errors for model

parameters, based on the Kenward-Roger (1997) approach.

dof_satterthwaite() and dof_ml1() approximate degrees of freedom

based on Satterthwaite's method or the "m-l-1" rule.

Examples

if (require("lme4", quietly = TRUE)) {

model <- lmer(Petal.Length ~ Sepal.Length + (1 | Species), data = iris)

p_value_kenward(model)

}

"m-l-1" approximation for SEs, CIs and p-values

Description

Approximation of degrees of freedom based on a "m-l-1" heuristic as suggested by Elff et al. (2019).

Usage

ci_ml1(model, ci = 0.95, ...)

dof_ml1(model)

p_value_ml1(model, dof = NULL, ...)

Arguments

model |

A mixed model. |

ci |

Confidence Interval (CI) level. Default to |

... |

Additional arguments passed down to the underlying functions.

E.g., arguments like |

dof |

Degrees of Freedom. |

Details

Small Sample Cluster corrected Degrees of Freedom

Inferential statistics (like p-values, confidence intervals and

standard errors) may be biased in mixed models when the number of clusters

is small (even if the sample size of level-1 units is high). In such cases

it is recommended to approximate a more accurate number of degrees of freedom

for such inferential statistics (see Li and Redden 2015). The

m-l-1 heuristic is such an approach that uses a t-distribution with

fewer degrees of freedom (dof_ml1()) to calculate p-values

(p_value_ml1()) and confidence intervals (ci(method = "ml1")).

Degrees of Freedom for Longitudinal Designs (Repeated Measures)

In particular for repeated measure designs (longitudinal data analysis),

the m-l-1 heuristic is likely to be more accurate than simply using the

residual or infinite degrees of freedom, because dof_ml1() returns

different degrees of freedom for within-cluster and between-cluster effects.

Limitations of the "m-l-1" Heuristic

Note that the "m-l-1" heuristic is not applicable (or at least less accurate)

for complex multilevel designs, e.g. with cross-classified clusters. In such cases,

more accurate approaches like the Kenward-Roger approximation (dof_kenward())

is recommended. However, the "m-l-1" heuristic also applies to generalized

mixed models, while approaches like Kenward-Roger or Satterthwaite are limited

to linear mixed models only.

Value

A data frame.

References

Elff, M.; Heisig, J.P.; Schaeffer, M.; Shikano, S. (2019). Multilevel Analysis with Few Clusters: Improving Likelihood-based Methods to Provide Unbiased Estimates and Accurate Inference, British Journal of Political Science.

Li, P., Redden, D. T. (2015). Comparing denominator degrees of freedom approximations for the generalized linear mixed model in analyzing binary outcome in small sample cluster-randomized trials. BMC Medical Research Methodology, 15(1), 38. doi:10.1186/s12874-015-0026-x

See Also

dof_ml1() is a small helper-function to calculate approximated

degrees of freedom of model parameters, based on the "m-l-1" heuristic.

Examples

if (require("lme4")) {

model <- lmer(Petal.Length ~ Sepal.Length + (1 | Species), data = iris)

p_value_ml1(model)

}

Satterthwaite approximation for SEs, CIs and p-values

Description

An approximate F-test based on the Satterthwaite (1946) approach.

Usage

ci_satterthwaite(model, ci = 0.95, ...)

dof_satterthwaite(model)

p_value_satterthwaite(model, dof = NULL, ...)

se_satterthwaite(model)

Arguments

model |

A statistical model. |

ci |

Confidence Interval (CI) level. Default to |

... |

Additional arguments passed down to the underlying functions.

E.g., arguments like |

dof |

Degrees of Freedom. |

Details

Inferential statistics (like p-values, confidence intervals and

standard errors) may be biased in mixed models when the number of clusters

is small (even if the sample size of level-1 units is high). In such cases

it is recommended to approximate a more accurate number of degrees of freedom

for such inferential statistics. Unlike simpler approximation heuristics

like the "m-l-1" rule (dof_ml1), the Satterthwaite approximation is

also applicable in more complex multilevel designs. However, the "m-l-1"

heuristic also applies to generalized mixed models, while approaches like

Kenward-Roger or Satterthwaite are limited to linear mixed models only.

Value

A data frame.

References

Satterthwaite FE (1946) An approximate distribution of estimates of variance components. Biometrics Bulletin 2 (6):110–4.

See Also

dof_satterthwaite() and se_satterthwaite() are small helper-functions

to calculate approximated degrees of freedom and standard errors for model

parameters, based on the Satterthwaite (1946) approach.

dof_kenward() and dof_ml1() approximate degrees of freedom based on

Kenward-Roger's method or the "m-l-1" rule.

Examples

if (require("lme4", quietly = TRUE)) {

model <- lmer(Petal.Length ~ Sepal.Length + (1 | Species), data = iris)

p_value_satterthwaite(model)

}

Cluster Analysis

Description

Compute hierarchical or kmeans cluster analysis and return the group assignment for each observation as vector.

Usage

cluster_analysis(

x,

n = NULL,

method = "kmeans",

include_factors = FALSE,

standardize = TRUE,

verbose = TRUE,

distance_method = "euclidean",

hclust_method = "complete",

kmeans_method = "Hartigan-Wong",

dbscan_eps = 15,

iterations = 100,

...

)

Arguments

x |

A data frame (with at least two variables), or a matrix (with at least two columns). |

n |

Number of clusters used for supervised cluster methods. If |

method |

Method for computing the cluster analysis. Can be |

include_factors |

Logical, if |

standardize |

Standardize the dataframe before clustering (default). |

verbose |

Toggle warnings and messages. |

distance_method |

Distance measure to be used for methods based on

distances (e.g., when |

hclust_method |

Agglomeration method to be used when |

kmeans_method |

Algorithm used for calculating kmeans cluster. Only applies,

if |

dbscan_eps |

The |

iterations |

The number of replications. |

... |

Arguments passed to or from other methods. |

Details

The print() and plot() methods show the (standardized) mean value for

each variable within each cluster. Thus, a higher absolute value indicates

that a certain variable characteristic is more pronounced within that

specific cluster (as compared to other cluster groups with lower absolute

mean values).

Clusters classification can be obtained via print(x, newdata = NULL, ...).

Value

The group classification for each observation as vector. The

returned vector includes missing values, so it has the same length

as nrow(x).

Note

There is also a plot()-method

implemented in the see-package.

References

Maechler M, Rousseeuw P, Struyf A, Hubert M, Hornik K (2014) cluster: Cluster Analysis Basics and Extensions. R package.

See Also

-

n_clusters()to determine the number of clusters to extract. -

cluster_discrimination()to determine the accuracy of cluster group classification via linear discriminant analysis (LDA). -

performance::check_clusterstructure()to check suitability of data for clustering. https://www.datanovia.com/en/lessons/

Examples

set.seed(33)

# K-Means ====================================================

rez <- cluster_analysis(iris[1:4], n = 3, method = "kmeans")

rez # Show results

predict(rez) # Get clusters

summary(rez) # Extract the centers values (can use 'plot()' on that)

if (requireNamespace("MASS", quietly = TRUE)) {

cluster_discrimination(rez) # Perform LDA

}

# Hierarchical k-means (more robust k-means)

if (require("factoextra", quietly = TRUE)) {

rez <- cluster_analysis(iris[1:4], n = 3, method = "hkmeans")

rez # Show results

predict(rez) # Get clusters

}

# Hierarchical Clustering (hclust) ===========================

rez <- cluster_analysis(iris[1:4], n = 3, method = "hclust")

rez # Show results

predict(rez) # Get clusters

# K-Medoids (pam) ============================================

if (require("cluster", quietly = TRUE)) {

rez <- cluster_analysis(iris[1:4], n = 3, method = "pam")

rez # Show results

predict(rez) # Get clusters

}

# PAM with automated number of clusters

if (require("fpc", quietly = TRUE)) {

rez <- cluster_analysis(iris[1:4], method = "pamk")

rez # Show results

predict(rez) # Get clusters

}

# DBSCAN ====================================================

if (require("dbscan", quietly = TRUE)) {

# Note that you can assimilate more outliers (cluster 0) to neighbouring

# clusters by setting borderPoints = TRUE.

rez <- cluster_analysis(iris[1:4], method = "dbscan", dbscan_eps = 1.45)

rez # Show results

predict(rez) # Get clusters

}

# Mixture ====================================================

if (require("mclust", quietly = TRUE)) {

library(mclust) # Needs the package to be loaded

rez <- cluster_analysis(iris[1:4], method = "mixture")

rez # Show results

predict(rez) # Get clusters

}

Find the cluster centers in your data

Description

For each cluster, computes the mean (or other indices) of the variables. Can be used to retrieve the centers of clusters. Also returns the within Sum of Squares.

Usage

cluster_centers(data, clusters, fun = mean, ...)

Arguments

data |

A data.frame. |

clusters |

A vector with clusters assignments (must be same length as rows in data). |

fun |

What function to use, |

... |

Other arguments to be passed to or from other functions. |

Value

A dataframe containing the cluster centers. Attributes include performance statistics and distance between each observation and its respective cluster centre.

Examples

k <- kmeans(iris[1:4], 3)

cluster_centers(iris[1:4], clusters = k$cluster)

cluster_centers(iris[1:4], clusters = k$cluster, fun = median)

Compute a linear discriminant analysis on classified cluster groups

Description

Computes linear discriminant analysis (LDA) on classified cluster groups, and

determines the goodness of classification for each cluster group. See MASS::lda()

for details.

Usage

cluster_discrimination(x, cluster_groups = NULL, ...)

Arguments

x |

A data frame |

cluster_groups |

Group classification of the cluster analysis, which can

be retrieved from the |

... |

Other arguments to be passed to or from. |

See Also

n_clusters() to determine the number of clusters to extract,

cluster_analysis() to compute a cluster analysis and

performance::check_clusterstructure() to check suitability of data for

clustering.

Examples

# Retrieve group classification from hierarchical cluster analysis

clustering <- cluster_analysis(iris[, 1:4], n = 3)

# Goodness of group classification

cluster_discrimination(clustering)

Metaclustering

Description

One of the core "issue" of statistical clustering is that, in many cases, different methods will give different results. The metaclustering approach proposed by easystats (that finds echoes in consensus clustering; see Monti et al., 2003) consists of treating the unique clustering solutions as a ensemble, from which we can derive a probability matrix. This matrix contains, for each pair of observations, the probability of being in the same cluster. For instance, if the 6th and the 9th row of a dataframe has been assigned to a similar cluster by 5 our of 10 clustering methods, then its probability of being grouped together is 0.5.

Usage

cluster_meta(list_of_clusters, rownames = NULL, ...)

Arguments

list_of_clusters |

A list of vectors with the clustering assignments from various methods. |

rownames |

An optional vector of row.names for the matrix. |

... |

Currently not used. |

Details

Metaclustering is based on the hypothesis that, as each clustering algorithm embodies a different prism by which it sees the data, running an infinite amount of algorithms would result in the emergence of the "true" clusters. As the number of algorithms and parameters is finite, the probabilistic perspective is a useful proxy. This method is interesting where there is no obvious reasons to prefer one over another clustering method, as well as to investigate how robust some clusters are under different algorithms.

This metaclustering probability matrix can be transformed into a dissimilarity

matrix (such as the one produced by dist()) and submitted for instance to

hierarchical clustering (hclust()). See the example below.

Value

A matrix containing all the pairwise (between each observation) probabilities of being clustered together by the methods.

Examples

data <- iris[1:4]

rez1 <- cluster_analysis(data, n = 2, method = "kmeans")

rez2 <- cluster_analysis(data, n = 3, method = "kmeans")

rez3 <- cluster_analysis(data, n = 6, method = "kmeans")

list_of_clusters <- list(rez1, rez2, rez3)

m <- cluster_meta(list_of_clusters)

# Visualize matrix without reordering

heatmap(m, Rowv = NA, Colv = NA, scale = "none") # Without reordering

# Reordered heatmap

heatmap(m, scale = "none")

# Extract 3 clusters

predict(m, n = 3)

# Convert to dissimilarity

d <- as.dist(abs(m - 1))

model <- hclust(d)

plot(model, hang = -1)

Performance of clustering models

Description

Compute performance indices for clustering solutions.

Usage

cluster_performance(model, ...)

## S3 method for class 'hclust'

cluster_performance(model, data, clusters, ...)

Arguments

model |

Cluster model. |

... |

Arguments passed to or from other methods. |

data |

A data frame. |

clusters |

A vector with clusters assignments (must be same length as rows in data). |

Examples

# kmeans

model <- kmeans(iris[1:4], 3)

cluster_performance(model)

# hclust

data <- iris[1:4]

model <- hclust(dist(data))

clusters <- cutree(model, 3)

cluster_performance(model, data, clusters)

# Retrieve performance from parameters

params <- model_parameters(kmeans(iris[1:4], 3))

cluster_performance(params)

Compare model parameters of multiple models

Description

Compute and extract model parameters of multiple regression

models. See model_parameters() for further details.

Usage

compare_parameters(

...,

ci = 0.95,

effects = "fixed",

component = "conditional",

standardize = NULL,

exponentiate = FALSE,

ci_method = "wald",

p_adjust = NULL,

select = NULL,

column_names = NULL,

pretty_names = TRUE,

coefficient_names = NULL,

keep = NULL,

drop = NULL,

include_reference = FALSE,

groups = NULL,

verbose = TRUE

)

compare_models(

...,

ci = 0.95,

effects = "fixed",

component = "conditional",

standardize = NULL,

exponentiate = FALSE,

ci_method = "wald",

p_adjust = NULL,

select = NULL,

column_names = NULL,

pretty_names = TRUE,

coefficient_names = NULL,

keep = NULL,

drop = NULL,

include_reference = FALSE,

groups = NULL,

verbose = TRUE

)

Arguments

... |

One or more regression model objects, or objects returned by

|

ci |

Confidence Interval (CI) level. Default to |

effects |

Should parameters for fixed effects ( |

component |

Model component for which parameters should be shown. See

documentation for related model class in |

standardize |

The method used for standardizing the parameters. Can be

|

exponentiate |

Logical, indicating whether or not to exponentiate the

coefficients (and related confidence intervals). This is typical for

logistic regression, or more generally speaking, for models with log or

logit links. It is also recommended to use |

ci_method |

Method for computing degrees of freedom for p-values

and confidence intervals (CI). See documentation for related model class

in |

p_adjust |

String value, if not |

select |

Determines which columns and and which layout columns are printed. There are three options for this argument:

For |

column_names |

Character vector with strings that should be used as

column headers. Must be of same length as number of models in |

pretty_names |

Can be |

coefficient_names |

Character vector with strings that should be used

as column headers for the coefficient column. Must be of same length as

number of models in |

keep |

Character containing a regular expression pattern that

describes the parameters that should be included (for |

drop |

See |

include_reference |

Logical, if |

groups |

Named list, can be used to group parameters in the printed output.

List elements may either be character vectors that match the name of those

parameters that belong to one group, or list elements can be row numbers

of those parameter rows that should belong to one group. The names of the

list elements will be used as group names, which will be inserted as "header

row". A possible use case might be to emphasize focal predictors and control

variables, see 'Examples'. Parameters will be re-ordered according to the

order used in |

verbose |

Toggle warnings and messages. |

Details

This function is in an early stage and does not yet cope with more complex models, and probably does not yet properly render all model components. It should also be noted that when including models with interaction terms, not only do the values of the parameters change, but so does their meaning (from main effects, to simple slopes), thereby making such comparisons hard. Therefore, you should not use this function to compare models with interaction terms with models without interaction terms.

Value

A data frame of indices related to the model's parameters.

Examples

data(iris)

lm1 <- lm(Sepal.Length ~ Species, data = iris)

lm2 <- lm(Sepal.Length ~ Species + Petal.Length, data = iris)

compare_parameters(lm1, lm2)

# custom style

compare_parameters(lm1, lm2, select = "{estimate}{stars} ({se})")

# custom style, in HTML

result <- compare_parameters(lm1, lm2, select = "{estimate}<br>({se})|{p}")

print_html(result)

data(mtcars)

m1 <- lm(mpg ~ wt, data = mtcars)

m2 <- glm(vs ~ wt + cyl, data = mtcars, family = "binomial")

compare_parameters(m1, m2)

# exponentiate coefficients, but not for lm

compare_parameters(m1, m2, exponentiate = "nongaussian")

# change column names

compare_parameters("linear model" = m1, "logistic reg." = m2)

compare_parameters(m1, m2, column_names = c("linear model", "logistic reg."))

# or as list

compare_parameters(list(m1, m2))

compare_parameters(list("linear model" = m1, "logistic reg." = m2))

Conversion between EFA results and CFA structure

Description

Enables a conversion between Exploratory Factor Analysis (EFA) and

Confirmatory Factor Analysis (CFA) lavaan-ready structure.

Usage

convert_efa_to_cfa(model, ...)

## S3 method for class 'fa'

convert_efa_to_cfa(

model,

threshold = "max",

names = NULL,

max_per_dimension = NULL,

...

)

efa_to_cfa(model, ...)

Arguments

model |

An EFA model (e.g., a |

... |

Arguments passed to or from other methods. |

threshold |

A value between 0 and 1 indicates which (absolute) values

from the loadings should be removed. An integer higher than 1 indicates the

n strongest loadings to retain. Can also be |

names |

Vector containing dimension names. |

max_per_dimension |

Maximum number of variables to keep per dimension. |

Value

Converted index.

Examples

library(parameters)

data(attitude)

efa <- psych::fa(attitude, nfactors = 3)

model1 <- efa_to_cfa(efa)

model2 <- efa_to_cfa(efa, threshold = 0.3)

model3 <- efa_to_cfa(efa, max_per_dimension = 2)

suppressWarnings(anova(

lavaan::cfa(model1, data = attitude),

lavaan::cfa(model2, data = attitude),

lavaan::cfa(model3, data = attitude)

))

Degrees of Freedom (DoF)

Description

Estimate or extract degrees of freedom of models parameters.

Usage

degrees_of_freedom(model, method = "analytical", ...)

dof(model, method = "analytical", ...)

Arguments

model |

A statistical model. |

method |

Type of approximation for the degrees of freedom. Can be one of the following:

Usually, when degrees of freedom are required to calculate p-values or

confidence intervals, |

... |

Currently not used. |

Note

In many cases, degrees_of_freedom() returns the same as df.residuals(),

or n-k (number of observations minus number of parameters). However,

degrees_of_freedom() refers to the model's parameters degrees of freedom

of the distribution for the related test statistic. Thus, for models with

z-statistic, results from degrees_of_freedom() and df.residuals() differ.

Furthermore, for other approximation methods like "kenward" or

"satterthwaite", each model parameter can have a different degree of

freedom.

Examples

model <- lm(Sepal.Length ~ Petal.Length * Species, data = iris)

dof(model)

model <- glm(vs ~ mpg * cyl, data = mtcars, family = "binomial")

dof(model)

model <- lmer(Sepal.Length ~ Petal.Length + (1 | Species), data = iris)

dof(model)

if (require("rstanarm", quietly = TRUE)) {

model <- stan_glm(

Sepal.Length ~ Petal.Length * Species,

data = iris,

chains = 2,

refresh = 0

)

dof(model)

}

Print tables in different output formats

Description

Prints tables (i.e. data frame) in different output formats.

print_md() is an alias for display(format = "markdown") and

print_html() is an alias for display(format = "html"). A third option is

display(format = "tt"), which returns a tinytable object, which is either

printed as markdown or HTML table, depending on the environment.

Usage

## S3 method for class 'parameters_model'

display(object, format = "markdown", ...)

Arguments

object |

An object returned by one of the package's function, for example

|

format |

String, indicating the output format. Can be |

... |

Arguments passed to the underlying functions, such as |

Details

display() is useful when the table-output from functions,

which is usually printed as formatted text-table to console, should

be formatted for pretty table-rendering in markdown documents, or if

knitted from rmarkdown to PDF or Word files. See

vignette

for examples.

Value

If format = "markdown", the return value will be a character

vector in markdown-table format. If format = "html", an object of

class gt_tbl. If format = "tt", an object of class tinytable.

See Also

print.parameters_model() and print.compare_parameters()

Examples

model <- lm(mpg ~ wt + cyl, data = mtcars)

mp <- model_parameters(model)

display(mp)

data(iris)

lm1 <- lm(Sepal.Length ~ Species, data = iris)

lm2 <- lm(Sepal.Length ~ Species + Petal.Length, data = iris)

lm3 <- lm(Sepal.Length ~ Species * Petal.Length, data = iris)

out <- compare_parameters(lm1, lm2, lm3)

print_html(

out,

select = "{coef}{stars}|({ci})",

column_labels = c("Estimate", "95% CI")

)

# line break, unicode minus-sign

print_html(

out,

select = "{estimate}{stars}<br>({ci_low} \u2212 {ci_high})",

column_labels = c("Est. (95% CI)")

)

data(iris)

data(Salamanders, package = "glmmTMB")

m1 <- lm(Sepal.Length ~ Species * Petal.Length, data = iris)

m2 <- lme4::lmer(

Sepal.Length ~ Petal.Length + Petal.Width + (1 | Species),

data = iris

)

m3 <- glmmTMB::glmmTMB(

count ~ spp + mined + (1 | site),

ziformula = ~mined,

family = poisson(),

data = Salamanders

)

out <- compare_parameters(m1, m2, m3, effects = "all", component = "all")

display(out, format = "tt")

display(out, select = "{estimate}|{ci}", format = "tt")

Dominance Analysis

Description

Computes Dominance Analysis Statistics and Designations

Usage

dominance_analysis(

model,

sets = NULL,

all = NULL,

conditional = TRUE,

complete = TRUE,

quote_args = NULL,

contrasts = model$contrasts,

...

)

Arguments

model |

A model object supported by |

sets |

A (named) list of formula objects with no left hand side/response. If the list has names, the name provided each element will be used as the label for the set. Unnamed list elements will be provided a set number name based on its position among the sets as entered. Predictors in each formula are bound together as a set in the dominance

analysis and dominance statistics and designations are computed for

the predictors together. Predictors in |

all |

A formula with no left hand side/response. Predictors in the formula are included in each subset in the dominance

analysis and the R2 value associated with them is subtracted from the

overall value. Predictors in |

conditional |

Logical. If If conditional dominance is not desired as an importance criterion, avoiding computing the conditional dominance matrix can save computation time. |

complete |

Logical. If If complete dominance is not desired as an importance criterion, avoiding computing complete dominance designations can save computation time. |

quote_args |

A character vector of arguments in the model submitted to

|

contrasts |

A named list of |

... |

Not used at current. |

Details

Computes two decompositions of the model's R2 and returns a matrix of designations from which predictor relative importance determinations can be obtained.

Note in the output that the "constant" subset is associated with a component of the model that does not directly contribute to the R2 such as an intercept. The "all" subset is apportioned a component of the fit statistic but is not considered a part of the dominance analysis and therefore does not receive a rank, conditional dominance statistics, or complete dominance designations.

The input model is parsed using insight::find_predictors(), does not

yet support interactions, transformations, or offsets applied in the R

formula, and will fail with an error if any such terms are detected.

The model submitted must accept an formula object as a formula

argument. In addition, the model object must accept the data on which

the model is estimated as a data argument. Formulas submitted

using object references (i.e., lm(mtcars$mpg ~ mtcars$vs)) and

functions that accept data as a non-data argument

(e.g., survey::svyglm() uses design) will fail with an error.

Models that return TRUE for the insight::model_info()

function's values "is_bayesian", "is_mixed", "is_gam",

is_multivariate", "is_zero_inflated",

or "is_hurdle" are not supported at current.

When performance::r2() returns multiple values, only the first is used

by default.

Value

Object of class "parameters_da".

An object of class "parameters_da" is a list of data.frames composed

of the following elements:

GeneralA

data.framewhich associates dominance statistics with model parameters. The variables in thisdata.frameinclude:ParameterParameter names.

General_DominanceVector of general dominance statistics. The R2 ascribed to variables in the

allargument are also reported here though they are not general dominance statistics.PercentVector of general dominance statistics normalized to sum to 1.

RanksVector of ranks applied to the general dominance statistics.

SubsetNames of the subset to which the parameter belongs in the dominance analysis. Each other

data.framereturned will refer to these subset names.

ConditionalA

data.frameof conditional dominance statistics. Each observation represents a subset and each variable represents an the average increment to R2 with a specific number of subsets in the model.NULLifconditionalargument isFALSE.CompleteA

data.frameof complete dominance designations. The subsets in the observations are compared to the subsets referenced in each variable. Whether the subset in each variable dominates the subset in each observation is represented in the logical value.NULLifcompleteargument isFALSE.

Author(s)

Joseph Luchman

References

Azen, R., & Budescu, D. V. (2003). The dominance analysis approach for comparing predictors in multiple regression. Psychological Methods, 8(2), 129-148. doi:10.1037/1082-989X.8.2.129

Budescu, D. V. (1993). Dominance analysis: A new approach to the problem of relative importance of predictors in multiple regression. Psychological Bulletin, 114(3), 542-551. doi:10.1037/0033-2909.114.3.542

Groemping, U. (2007). Estimators of relative importance in linear regression based on variance decomposition. The American Statistician, 61(2), 139-147. doi:10.1198/000313007X188252

See Also

Examples

data(mtcars)

# Dominance Analysis with Logit Regression

model <- glm(vs ~ cyl + carb + mpg, data = mtcars, family = binomial())

performance::r2(model)

dominance_analysis(model)

# Dominance Analysis with Weighted Logit Regression

model_wt <- glm(vs ~ cyl + carb + mpg,

data = mtcars,

weights = wt, family = quasibinomial()

)

dominance_analysis(model_wt, quote_args = "weights")

Equivalence test

Description

Compute the (conditional) equivalence test for frequentist models.

Usage

## S3 method for class 'lm'

equivalence_test(

x,

range = "default",

ci = 0.95,

rule = "classic",

effects = "fixed",

vcov = NULL,

vcov_args = NULL,

verbose = TRUE,

...

)

Arguments

x |

A statistical model. |

range |

The range of practical equivalence of an effect. May be

|

ci |

Confidence Interval (CI) level. Default to |

rule |

Character, indicating the rules when testing for practical

equivalence. Can be |

effects |

Should parameters for fixed effects ( |

vcov |

Variance-covariance matrix used to compute uncertainty estimates (e.g., for robust standard errors). This argument accepts a covariance matrix, a function which returns a covariance matrix, or a string which identifies the function to be used to compute the covariance matrix.

|

vcov_args |

List of arguments to be passed to the function identified by

the |

verbose |

Toggle warnings and messages. |

... |

Arguments passed to or from other methods. |

Details

In classical null hypothesis significance testing (NHST) within a

frequentist framework, it is not possible to accept the null hypothesis, H0 -

unlike in Bayesian statistics, where such probability statements are

possible. "... one can only reject the null hypothesis if the test

statistics falls into the critical region(s), or fail to reject this

hypothesis. In the latter case, all we can say is that no significant effect

was observed, but one cannot conclude that the null hypothesis is true."

(Pernet 2017). One way to address this issues without Bayesian methods is

Equivalence Testing, as implemented in equivalence_test(). While you

either can reject the null hypothesis or claim an inconclusive result in

NHST, the equivalence test - according to Pernet - adds a third category,

"accept". Roughly speaking, the idea behind equivalence testing in a

frequentist framework is to check whether an estimate and its uncertainty

(i.e. confidence interval) falls within a region of "practical equivalence".

Depending on the rule for this test (see below), statistical significance

does not necessarily indicate whether the null hypothesis can be rejected or

not, i.e. the classical interpretation of the p-value may differ from the

results returned from the equivalence test.

Calculation of equivalence testing

"bayes" - Bayesian rule (Kruschke 2018)

This rule follows the "HDI+ROPE decision rule" (Kruschke, 2014, 2018) used for the

Bayesian counterpart(). This means, if the confidence intervals are completely outside the ROPE, the "null hypothesis" for this parameter is "rejected". If the ROPE completely covers the CI, the null hypothesis is accepted. Else, it's undecided whether to accept or reject the null hypothesis. Desirable results are low proportions inside the ROPE (the closer to zero the better)."classic" - The TOST rule (Lakens 2017)

This rule follows the "TOST rule", i.e. a two one-sided test procedure (Lakens 2017). Following this rule...

practical equivalence is assumed (i.e. H0 "accepted") when the narrow confidence intervals are completely inside the ROPE, no matter if the effect is statistically significant or not;

practical equivalence (i.e. H0) is rejected, when the coefficient is statistically significant, both when the narrow confidence intervals (i.e.

1-2*alpha) include or exclude the the ROPE boundaries, but the narrow confidence intervals are not fully covered by the ROPE;else the decision whether to accept or reject practical equivalence is undecided (i.e. when effects are not statistically significant and the narrow confidence intervals overlaps the ROPE).

"cet" - Conditional Equivalence Testing (Campbell/Gustafson 2018)

The Conditional Equivalence Testing as described by Campbell and Gustafson 2018. According to this rule, practical equivalence is rejected when the coefficient is statistically significant. When the effect is not significant and the narrow confidence intervals are completely inside the ROPE, we accept (i.e. assume) practical equivalence, else it is undecided.

Levels of Confidence Intervals used for Equivalence Testing

For rule = "classic", "narrow" confidence intervals are used for

equivalence testing. "Narrow" means, the the intervals is not 1 - alpha,

but 1 - 2 * alpha. Thus, if ci = .95, alpha is assumed to be 0.05

and internally a ci-level of 0.90 is used. rule = "cet" uses

both regular and narrow confidence intervals, while rule = "bayes"

only uses the regular intervals.

p-Values

The equivalence p-value is the area of the (cumulative) confidence distribution that is outside of the region of equivalence. It can be interpreted as p-value for rejecting the alternative hypothesis and accepting the "null hypothesis" (i.e. assuming practical equivalence). That is, a high p-value means we reject the assumption of practical equivalence and accept the alternative hypothesis.

Second Generation p-Value (SGPV)

Second generation p-values (SGPV) were proposed as a statistic that represents the proportion of data-supported hypotheses that are also null hypotheses (Blume et al. 2018, Lakens and Delacre 2020). It represents the proportion of the full confidence interval range (assuming a normally or t-distributed, equal-tailed interval, based on the model) that is inside the ROPE. The SGPV ranges from zero to one. Higher values indicate that the effect is more likely to be practically equivalent ("not of interest").

Note that the assumed interval, which is used to calculate the SGPV, is an estimation of the full interval based on the chosen confidence level. For example, if the 95% confidence interval of a coefficient ranges from -1 to 1, the underlying full (normally or t-distributed) interval approximately ranges from -1.9 to 1.9, see also following code:

# simulate full normal distribution out <- bayestestR::distribution_normal(10000, 0, 0.5) # range of "full" distribution range(out) # range of 95% CI round(quantile(out, probs = c(0.025, 0.975)), 2)

This ensures that the SGPV always refers to the general compatible parameter space of coefficients, independent from the confidence interval chosen for testing practical equivalence. Therefore, the SGPV of the full interval is similar to the ROPE coverage of Bayesian equivalence tests, see following code:

library(bayestestR) library(brms) m <- lm(mpg ~ gear + wt + cyl + hp, data = mtcars) m2 <- brm(mpg ~ gear + wt + cyl + hp, data = mtcars) # SGPV for frequentist models equivalence_test(m) # similar to ROPE coverage of Bayesian models equivalence_test(m2) # similar to ROPE coverage of simulated draws / bootstrap samples equivalence_test(simulate_model(m))

ROPE range

Some attention is required for finding suitable values for the ROPE limits

(argument range). See 'Details' in bayestestR::rope_range()

for further information.

Value

A data frame.

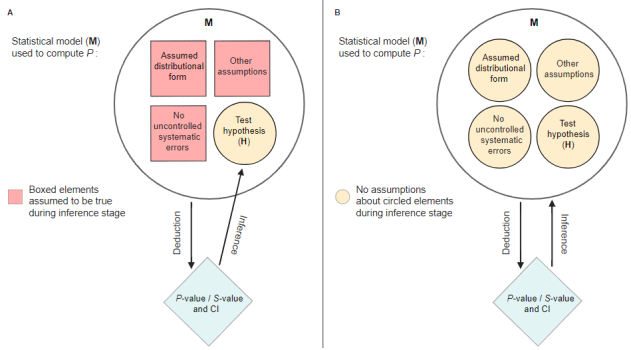

Statistical inference - how to quantify evidence

There is no standardized approach to drawing conclusions based on the available data and statistical models. A frequently chosen but also much criticized approach is to evaluate results based on their statistical significance (Amrhein et al. 2017).

A more sophisticated way would be to test whether estimated effects exceed the "smallest effect size of interest", to avoid even the smallest effects being considered relevant simply because they are statistically significant, but clinically or practically irrelevant (Lakens et al. 2018, Lakens 2024).

A rather unconventional approach, which is nevertheless advocated by various authors, is to interpret results from classical regression models either in terms of probabilities, similar to the usual approach in Bayesian statistics (Schweder 2018; Schweder and Hjort 2003; Vos 2022) or in terms of relative measure of "evidence" or "compatibility" with the data (Greenland et al. 2022; Rafi and Greenland 2020), which nevertheless comes close to a probabilistic interpretation.

A more detailed discussion of this topic is found in the documentation of

p_function().

The parameters package provides several options or functions to aid statistical inference. These are, for example:

-

equivalence_test(), to compute the (conditional) equivalence test for frequentist models -

p_significance(), to compute the probability of practical significance, which can be conceptualized as a unidirectional equivalence test -

p_function(), or consonance function, to compute p-values and compatibility (confidence) intervals for statistical models the

pdargument (settingpd = TRUE) inmodel_parameters()includes a column with the probability of direction, i.e. the probability that a parameter is strictly positive or negative. SeebayestestR::p_direction()for details. If plotting is desired, thep_direction()function can be used, together withplot().the

s_valueargument (settings_value = TRUE) inmodel_parameters()replaces the p-values with their related S-values (Rafi and Greenland 2020)finally, it is possible to generate distributions of model coefficients by generating bootstrap-samples (setting

bootstrap = TRUE) or simulating draws from model coefficients usingsimulate_model(). These samples can then be treated as "posterior samples" and used in many functions from the bayestestR package.

Most of the above shown options or functions derive from methods originally

implemented for Bayesian models (Makowski et al. 2019). However, assuming

that model assumptions are met (which means, the model fits well to the data,

the correct model is chosen that reflects the data generating process

(distributional model family) etc.), it seems appropriate to interpret

results from classical frequentist models in a "Bayesian way" (more details:

documentation in p_function()).

Note

There is also a plot()-method

implemented in the see-package.

References

Amrhein, V., Korner-Nievergelt, F., and Roth, T. (2017). The earth is flat (p > 0.05): Significance thresholds and the crisis of unreplicable research. PeerJ, 5, e3544. doi:10.7717/peerj.3544

Blume, J. D., D'Agostino McGowan, L., Dupont, W. D., & Greevy, R. A. (2018). Second-generation p-values: Improved rigor, reproducibility, & transparency in statistical analyses. PLOS ONE, 13(3), e0188299. https://doi.org/10.1371/journal.pone.0188299

Campbell, H., & Gustafson, P. (2018). Conditional equivalence testing: An alternative remedy for publication bias. PLOS ONE, 13(4), e0195145. doi: 10.1371/journal.pone.0195145

Greenland S, Rafi Z, Matthews R, Higgs M. To Aid Scientific Inference, Emphasize Unconditional Compatibility Descriptions of Statistics. (2022) https://arxiv.org/abs/1909.08583v7 (Accessed November 10, 2022)

Kruschke, J. K. (2014). Doing Bayesian data analysis: A tutorial with R, JAGS, and Stan. Academic Press

Kruschke, J. K. (2018). Rejecting or accepting parameter values in Bayesian estimation. Advances in Methods and Practices in Psychological Science, 1(2), 270-280. doi: 10.1177/2515245918771304

Lakens, D. (2017). Equivalence Tests: A Practical Primer for t Tests, Correlations, and Meta-Analyses. Social Psychological and Personality Science, 8(4), 355–362. doi: 10.1177/1948550617697177

Lakens, D. (2024). Improving Your Statistical Inferences (Version v1.5.1). Retrieved from https://lakens.github.io/statistical_inferences/. doi:10.5281/ZENODO.6409077

Lakens, D., and Delacre, M. (2020). Equivalence Testing and the Second Generation P-Value. Meta-Psychology, 4. https://doi.org/10.15626/MP.2018.933

Lakens, D., Scheel, A. M., and Isager, P. M. (2018). Equivalence Testing for Psychological Research: A Tutorial. Advances in Methods and Practices in Psychological Science, 1(2), 259–269.

Makowski, D., Ben-Shachar, M. S., Chen, S. H. A., and Lüdecke, D. (2019). Indices of Effect Existence and Significance in the Bayesian Framework. Frontiers in Psychology, 10, 2767. doi:10.3389/fpsyg.2019.02767

Pernet, C. (2017). Null hypothesis significance testing: A guide to commonly misunderstood concepts and recommendations for good practice. F1000Research, 4, 621. doi: 10.12688/f1000research.6963.5

Rafi Z, Greenland S. Semantic and cognitive tools to aid statistical science: replace confidence and significance by compatibility and surprise. BMC Medical Research Methodology (2020) 20:244.

Schweder T. Confidence is epistemic probability for empirical science. Journal of Statistical Planning and Inference (2018) 195:116–125. doi:10.1016/j.jspi.2017.09.016

Schweder T, Hjort NL. Frequentist analogues of priors and posteriors. In Stigum, B. (ed.), Econometrics and the Philosophy of Economics: Theory Data Confrontation in Economics, pp. 285-217. Princeton University Press, Princeton, NJ, 2003

Vos P, Holbert D. Frequentist statistical inference without repeated sampling. Synthese 200, 89 (2022). doi:10.1007/s11229-022-03560-x

See Also

For more details, see bayestestR::equivalence_test(). Further

readings can be found in the references. See also p_significance() for

a unidirectional equivalence test.

Examples

data(qol_cancer)

model <- lm(QoL ~ time + age + education, data = qol_cancer)

# default rule

equivalence_test(model)

# using heteroscedasticity-robust standard errors

equivalence_test(model, vcov = "HC3")

# conditional equivalence test

equivalence_test(model, rule = "cet")

# plot method

if (require("see", quietly = TRUE)) {

result <- equivalence_test(model)

plot(result)

}

Principal Component Analysis (PCA) and Factor Analysis (FA)

Description

The functions principal_components() and factor_analysis() can be used to

perform a principal component analysis (PCA) or a factor analysis (FA). They

return the loadings as a data frame, and various methods and functions are

available to access / display other information (see the 'Details' section).

Usage

factor_analysis(x, ...)

## S3 method for class 'data.frame'

factor_analysis(

x,

n = "auto",

rotation = "oblimin",

factor_method = "minres",

sort = FALSE,

threshold = NULL,

standardize = FALSE,

...

)

## S3 method for class 'matrix'

factor_analysis(

x,

n = "auto",

rotation = "oblimin",

factor_method = "minres",

n_obs = NULL,

sort = FALSE,

threshold = NULL,

standardize = FALSE,

...

)

principal_components(x, ...)

rotated_data(x, verbose = TRUE)

## S3 method for class 'data.frame'

principal_components(

x,

n = "auto",

rotation = "none",

sparse = FALSE,

sort = FALSE,

threshold = NULL,

standardize = TRUE,

...

)

## S3 method for class 'parameters_efa'

print_html(x, digits = 2, threshold = NULL, labels = NULL, ...)

## S3 method for class 'parameters_efa'

predict(

object,

newdata = NULL,

names = NULL,

keep_na = TRUE,

verbose = TRUE,

...

)

## S3 method for class 'parameters_efa'

print(x, digits = 2, threshold = NULL, labels = NULL, ...)

## S3 method for class 'parameters_efa'

sort(x, ...)

closest_component(x)

Arguments

x |

A data frame or a statistical model. For |

... |

Arguments passed to or from other methods. |

n |

Number of components to extract. If |

rotation |

If not |

factor_method |

The factoring method to be used. Passed to the |

sort |

Sort the loadings. |

threshold |

A value between 0 and 1 indicates which (absolute) values

from the loadings should be removed. An integer higher than 1 indicates the

n strongest loadings to retain. Can also be |

standardize |

A logical value indicating whether the variables should be

standardized (centered and scaled) to have unit variance before the

analysis (in general, such scaling is advisable). Note: This defaults

to |

n_obs |

An integer or a matrix.

|

verbose |

Toggle warnings. |

sparse |

Whether to compute sparse PCA (SPCA, using |

digits |

Argument for |

labels |

Argument for |

object |

An object of class |

newdata |

An optional data frame in which to look for variables with which to predict. If omitted, the fitted values are used. |

names |

Optional character vector to name columns of the returned data frame. |

keep_na |

Logical, if |

Details

Methods and Utilities

-

n_components()andn_factors()automatically estimates the optimal number of dimensions to retain. -

performance::check_factorstructure()checks the suitability of the data for factor analysis using the sphericity (seeperformance::check_sphericity_bartlett()) and the KMO (seeperformance::check_kmo()) measure. -

performance::check_itemscale()computes various measures of internal consistencies applied to the (sub)scales (i.e., components) extracted from the PCA. Running

summary()returns information related to each component/factor, such as the explained variance and the Eivenvalues.Running

get_scores()computes scores for each subscale.-

factor_scores()extracts the factor scores from objects returned bypsych::fa(),factor_analysis(), orpsych::omega(). Running

closest_component()will return a numeric vector with the assigned component index for each column from the original data frame.Running

rotated_data()will return the rotated data, including missing values, so it matches the original data frame.-

performance::item_omega()is a convenient wrapper aroundpsych::omega(), which provides some additional methods to work seamlessly within the easystats framework. -

performance::check_normality()checks residuals from objects returned bypsych::fa(),factor_analysis(),performance::item_omega(), orpsych::omega()for normality. -

performance::model_performance()returns fit-indices for objects returned bypsych::fa(),factor_analysis(), orpsych::omega(). Running

plot()visually displays the loadings (that requires the see-package to work).

Complexity

Complexity represents the number of latent components needed to account for the observed variables. Whereas a perfect simple structure solution has a complexity of 1 in that each item would only load on one factor, a solution with evenly distributed items has a complexity greater than 1 (Hofman, 1978; Pettersson and Turkheimer, 2010).

Uniqueness

Uniqueness represents the variance that is 'unique' to the variable and

not shared with other variables. It is equal to 1 - communality

(variance that is shared with other variables). A uniqueness of 0.20

suggests that 20% or that variable's variance is not shared with other

variables in the overall factor model. The greater 'uniqueness' the lower

the relevance of the variable in the factor model.

MSA